CHAI is pleased to release the 2026 Hepatitis C Treatment Market Memo, the latest in our series of hepatitis C market intelligence publications.

A decade ago, curing hepatitis C cost more than US$84,000 per patient. Today, the same cure can be procured at around US$60 per patient. Few global health markets have changed so dramatically. Yet despite this transformation, millions of people who have already been diagnosed with hepatitis C still cannot access treatment. Countries like Rwanda have demonstrated that national-scale elimination is achievable: over 10 million people screened, prevalence reduced to below 1 percent, and moving toward WHO path-to-elimination validation.

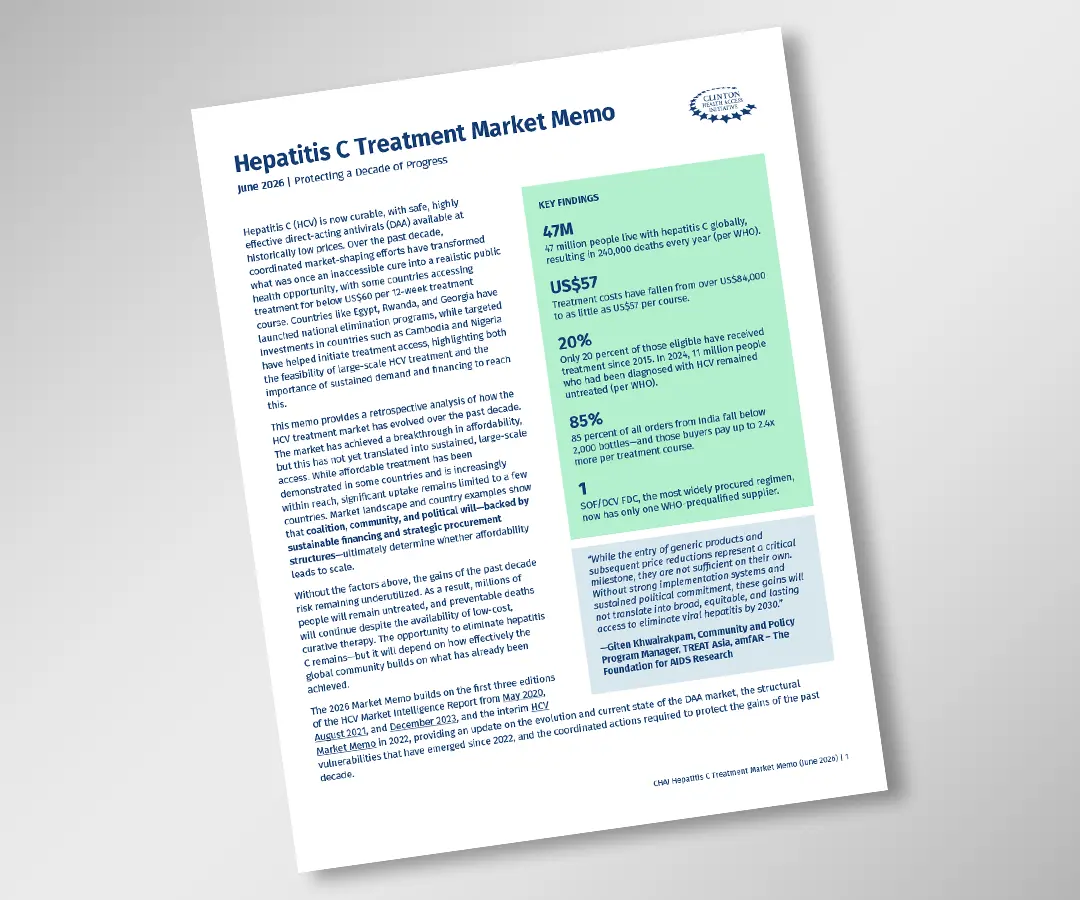

Yet only 20 percent of those eligible have received treatment since 2015, and in 2024, 11 million people who had been diagnosed with hepatitis C remained untreated. Treatment has become more affordable. But the financing and coordinated demand needed to sustain the market have not followed.

What this edition adds

Previous editions of this series tracked aggregated trends across low- and middle-income countries in supply, pricing, and procurement volumes. This edition goes further. For the first time, we draw on India’s generic export database to examine country-level procurement patterns in Cambodia, Nigeria, Rwanda, and Vietnam, showing how financing structures, procurement architecture, and policy choices at the country level determine whether affordable prices translate into patient access. It captures not just what prices have been achieved globally, but why some countries convert affordability into access and others do not.

Building on prior editions, this memo updates the price-volume analysis across all main DAA regimens. The data is stark: 85 percent of all India export orders fall below 2,000 bottles, and buyers pay up to 2.4 times more per treatment course than those ordering at scale.

Looking ahead

Protecting the progress of the past decade will require coordinated action. Governments that consolidate procurement and commit to multi-year financing achieve better prices and more durable supplier engagement, as Cambodia, Nigeria, and Rwanda each illustrate. Sharing procurement data across agencies would enable the demand aggregation that market stability requires. The supply base for the most affordable regimens is narrowing, with SOF/DCV FDC now having only one WHO PQ supplier. Civil society advocacy remains critical to sustaining political attention on hepatitis C and the domestic financing that programs depend on.

The window to consolidate the gains of the past decade is narrowing. The tools, the evidence, and the prices still exist. What is needed now is the coordination to use them.

CHAI would like to thank the World Health Organization and the Medicines Patent Pool for their review of this edition, and Giten Khwairakpam (TREAT Asia, amfAR) and Danjuma Adda (Centre for Initiative and Development, Nigeria) for contributing community perspectives.

This memo is the latest in CHAI’s ongoing effort to build market transparency for hepatitis C commodities. Previous editions: 1st Edition (May 2020), 2nd Edition (August 2021), Market Memo (July 2022), 3rd Edition (2023).